How To Build Your 3-Fund Portfolio

Jack Bogle, the father of index funds is famous for saying:

“Simplicity is the master key to financial success.” - Jack Bogle

And there is no simpler, and effective investment portfolio than the 3-fund portfolio. By owning just three simple low-cost index funds, a Total U.S. Equity, a Total U.S. Bond, and a Total International Equity, all of us can outperform the vast majority of mutual funds out there. In this post I’m going to walk you through step by step on building your own 3-fund portfolio.

The Simple 3-Fund Portfolio

Step 1 - Fund Selection

The first step to building our 3-fund portfolio is to gather our ingredients. And in this case, it would be our three low cost index funds. One to represent the US equities market. One to represent the bonds market. And one to represent the international equities market.

US Equities Fund - VTSAX

As regards to the US equities market, my personal favorite is the Vanguard Total Stock Market Index Fund, also known as VTSAX. Introduced in 1992, this one fund allows investors to own more than 4,000 publicly traded U.S. companies at an extremely low cost. VTSAX tracks the CRSP US Total Market Index. CRSP stands for Center for Research in Security Prices and is part of University of Chicago’s Booth School of Business.

It probably is the most comprehensible total market index that includes around 4,000 companies across mega, large, small and micro capitalization. There is a minimum investment of $3,000 and an expense ratio of 0.04%. Putting this in dollars means that an investor can invest $10,000 into VTSAX at a cost of only $4 per year. An alternate equities fund you can also hold is Vanguard 500 Index Fund, also known as VFIAX.

While VTSAX owns every US company out there, the Vanguard 500 holds only the 500 largest publicly traded companies. The difference of 3,500 companies may sound like a lot, but in actuality VTSAX and VFIAX are actually a lot more similar than different. And this is due to market capitalization.

Market capitalization refers to the total dollar market value of a company. Its size is based on the number of shares and the current market price of each share. Oftentimes, bigger the company, bigger its market capitalization. At the time of this post, the biggest companies in the United States based on market cap are Apple, Microsoft and Amazon.

Therefore, the 500 largest publicly traded companies, given their sheer size, represent 80 to 85% of the market. So if you prefer to hold the largest companies as your core equities holding, VFIAX is a great alternative to VTSAX.

US Bond Fund - VBTLX

The second fund you want to hold in your 3-fund portfolio is one to represent the bond market. And my favorite in this category is the Vanguard Total Bond Market Index Fund also known as VBTLX. This one fund allows investors to own more than 10,000 very diversified, high-quality U.S. investment grade bonds.

The VBTLX tracks the Bloomberg U.S. Aggregate Float Adjusted Index. A broad-based benchmark that measures the investment grade, US dollar-denominated, fixed-rate taxable bond market. In simplest terms, this one fund is designed to provide broad exposure to the U.S. investment-grade bond market. There is a minimum investment of $3,000 and an expense ratio of 0.05%. Putting this in dollars means that an investor can invest $10,000 into VBTLX at a cost of only $5 per year.

International Fund - VTIAX

The third fund you want to hold in your 3-fund portfolio is one to represent the international market. And my favorite in this category is Vanguard Total International Stock Index Fund also known as VTIAX. This one fund offers investors a low cost way to gain equity exposure to both developed and emerging international economies. It holds more than 7,000 international stocks from developed countries like England and France as well as from emerging countries like China and Brazil.

It includes major international companies like Taiwan Semiconductor Manufacturing, Nestle and Samsung. The fund tracks stock markets all over the globe, with the exception of the United States following the FTSE Global All Cap ex US Index. There is a minimum investment of $3,000 and an expense ratio of 0.11%. Putting this in dollars means that an investor can invest $10,000 into VTIAX at a cost of only $11 per year.

So to summarize, if your investment firm is Vanguard, consider the following three funds for your 3 fund portfolio:

Before I move onto step 2, I do want to share some alternate options, specifically if your preferred investment firm is Fidelity.

FZROX

To represent your equities holding, I would recommend the Fidelity Zero Total Market Index Fund. Also known as FZROX. The fund tracks Fidelity’s inhouse, Fidelity U.S. Total Investable Market Index and it represents approximately 2,661 US based companies.

Compared to VTSAX, it excludes certain companies based on market capitalization. Essentially, smaller companies. However I wouldn't concern myself too much about this difference given when looking at it from the perspective of market capitalization, the excluded companies represent less than 1% of the fund. Similar to VTSAX, the top holdings in this fund are Apple, Microsoft and Amazon.

The nice thing about FZROX is that it has an expense ratio of 0.00%. Yes you heard me right. $0 dollars to invest in Fidelity Zero Total Market Index Fund. Thus the zero in its name. But a quick thing to note about Fidelity Zero Total Market Index Fund is the fact that you can’t transfer your shares of FZROX to another firm without selling your holding. And when you sell your holdings, you have to pay taxes on your capital gains.

The Fidelity Zero Total Market Index Fund was designed with a 0% expense ratio in order to gain more customers. So Fidelity doesn’t want you to move your money to a different firm and this limitation creates that barrier. If this limitation concerns you, you might want to consider looking at Fidelity Total Market Index Fund, FSKAX. It has an expense ratio of 0.015%, but does provide more flexibility than the FZROX if that is what you are looking for.

FXNAX

Moving on, to represent your bond fund, I would recommend Fidelity U.S. Bond Index Fund, also known as FXNAX. It tracks the Bloomberg Barclays U.S. Aggregate Bond Index which is composed of investment-grade government bonds, corporate bonds and mortgage backed securities. It holds approximately 8,430 bonds. The top issuers are the US Treasury or issuers of Mortgage Backed securities like Fannie Mae and Freddie Mac. It has an expense ratio of 0.025%. Which means if you have $10,000 invested in Fidelity U.S. Bond Index Fund, you are essentially paying $2.50 for Fidelity to manage this fund for you.

FTIHX

To represent your international fund, I would recommend Fidelity Total International Index Fund, FTIHX. The fund tracks the MSCI All Country World Index excluding the United States. It represents approximately 5,042 international companies from both developed and emerging markets like the VTIAX. The top holdings in this fund are made up of companies like Taiwan Semiconductor, Nestle and ASML holdings. It has an expense ratio of 0.06%. Which means if you have $10,000 invested in FTIHX, you are essentially paying $6.00 for Fidelity to manage this fund for you.

Step 2 - Asset Allocation

Alright, now that you have your core ingredients, your index funds, let’s talk about asset allocation which is step 2 to building your 3-fund portfolio. In this step, we want to identify how much of each fund we want in our portfolio. After identifying your specific index funds, I would say this is the most important investment decision. I say this because, with the exception of the amount you are saving and investing, your asset allocation, your stock to bond ratio, determines your expected risk, and therefore your expected long term returns.

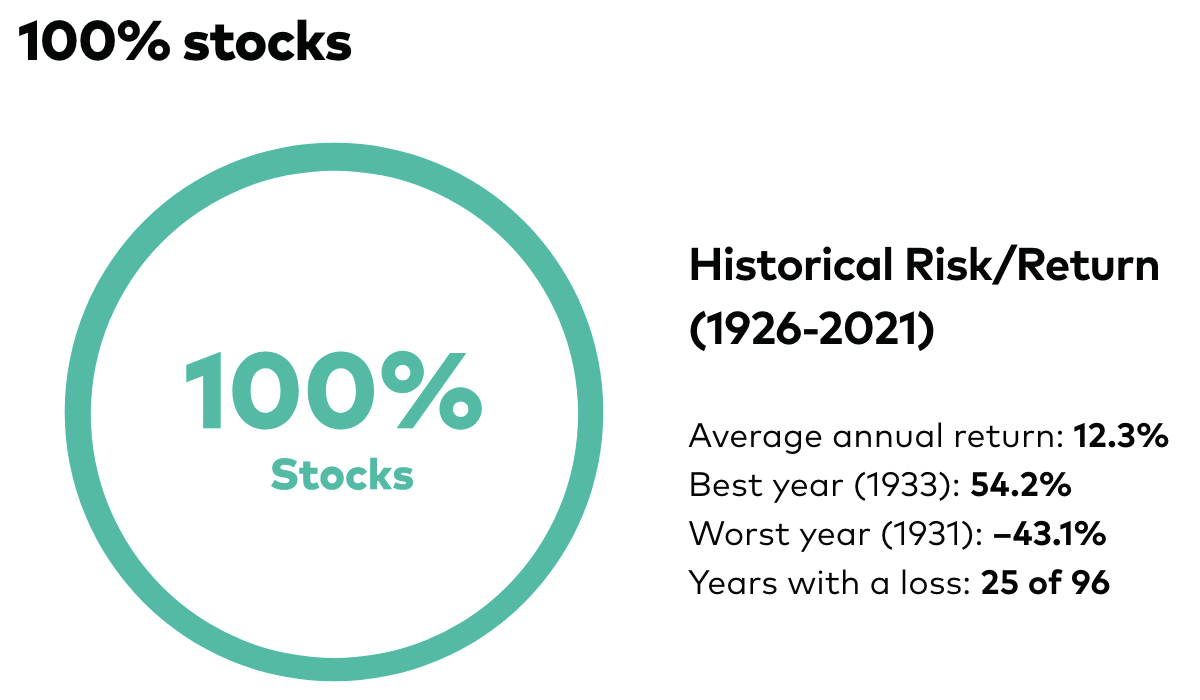

It is very important to understand that risk and returns go hand in hand. The higher the expected return, the higher the expected risk. If we want greater returns in our portfolio, we must get comfortable with greater risk. And our stock to bond allocation is a mechanism to control that risk level. Vanguard research shows the average annual return and the worst single year return of various stock to bond allocation from 1926 to 2021.

Let’s say that we went 100% stocks. Assuming the most risky asset allocation we can. The average annual return would be 12.3%. But in our worst year, we would have lost 43.1% of our portfolio. This means if we had a $100,000 portfolio, in a single year, we could see our portfolio lose up to $43,000 dollars in value. This could be hard to swallow for many people. Especially if you were expecting to pull some of that money out soon.

So let’s say we decided to go 100% bonds. Assuming the least risky asset allocation that we can. In our worst year, we would have only lost 8.1% of our portfolio. Which is much better than 43.1% from our 100% stock portfolio. However, our average annual return is only 6.3%. Half what we would have gotten compared to the 100% stock portfolio. We took less risk by going with 100% bonds, but we also got less returns.

The reality is that most of us probably fall somewhere in between. So we must find our ideal asset allocation that aligns with our risk tolerance. We may not be so risky that we go 100% in stocks at all times, but we also may not be so risk averse to have all our money in 100% bonds.

There is a lot that you want to consider in determining your risk tolerance such as your current income, when you plan to retire and your financial goals. We won’t have time to dive into all of them in this post, but if you like to spend the time to determine your own personal risk tolerance, check out my post here. For now, to help you identify your starting place, let me share with you a few examples:

Sample Asset Allocations

Aggressive - If you are aggressive with your risk tolerance. Meaning you actually embrace volatility and have a long time horizon for your investment, a 90/10 Stock to Bond ratio might be ok for you. You might even be able to push it to 100% in stocks if you really want to be aggressive. And if you are in your 20s or even 30s, I would actually recommend this given you have time on your side. When you are young, risk is your friend. Don’t shy away from it. Market will always have its ups and downs, but if you have time on your side, most often your portfolio will fully recover within a few years.

Moderate - Now, let’s say that you are more moderate with your risk tolerance. Meaning, you are ok with volatility, but because maybe you have a large family or your income isn’t as consistent, you don’t want to be so risky. Here, a 80/20 or 70/30 stocks to bond ratio might be best. You have enough stocks to take advantage of the market, but also enough bonds to smooth out the ride. If you are in your 40s or 50s, you might be in this bucket.

Conservative - Alright, let’s say you are conservative with your risk tolerance. You are in the later stages of life so retirement is right around the corner. You don’t need to become ultra rich in your lifetime. You have your lifestyle and you just need the ability to fund it. In this case, a 60/40 or even 40/60 stock to bond ratio might be a good option. You can taper your bond up or down based on how conservative you are.

One thing I want to call out is that in these examples we don’t talk about international stocks. How much of our stocks should we allocate to Vanguard Total International Stock Index Fund or Fidelity Total International Index Fund? I know the examples here don't specifically call out the percentage of stock allocation that should be invested in international stocks.

To be honest, this is one of the most controversial subjects in investing. There are constant arguments for more international funds versus less international funds. And both sides of the argument make sense. We don’t have time to delve into all the details of the argument in this video, so if you like to learn more check out my video here.

But let me at least share with you my personal recommendation and what I do. My personal recommendation is that around 20% should be fine for most investors. Jack Bogle suggests up to 20% and Vanguard studies recommend minimum 20%. So in general 20% of your stock allocation in international stocks is a good compromise. So how this is how it would look in a 80/20 stock to bond asset allocation.

60% in Vanguard Total Stock Market Index Fund, VTSAX.

20% in Vanguard Total International Stock Index Fund, VTIAX.

20% in Vanguard Total Bond Market Index Fund, VBTLX.

And know that asset allocation is a fluid concept. As your life situation changes, so should your asset allocation to align with your new risk tolerance.

Step 3 - Tax Optimization

Alright, let’s move to step three. Optimizing taxes. So far we’ve identified the specific index fund and the appropriate asset allocation. However, in order to optimize our investments. Meaning minimizing tax treatment, we must also determine where to hold our investments. This is essentially understanding which investments go in what accounts. And when I’m talking about accounts, I’m referring to buckets that hold the specific index fund investments. Commonly known accounts like 401(k), IRA and taxable brokerage accounts.

Two Types of Accounts - Tax Advantaged & Ordinary

In general, there are two types of accounts that we should be aware of. Tax advantaged accounts or ordinary accounts. Tax Advantaged Accounts are commonly known retirement vehicles such as 401(k), Roth IRA and Traditional IRA.

In the United States, the government taxes dividends, interest and capital gains on our investments. But it has also created several tax-advantaged accounts to encourage retirement savings. Thus when we hold money in these accounts, the Internal Revenue Service gives us tax benefits in forms of tax deferment or tax free withdrawals depending on the type of account.

A general rule of thumb is that no matter what financial situation we are in, we always want to take full advantage of all tax advantaged accounts offered to us. Ordinary accounts on the other hand are accounts that are not part of any tax-advantaged plan. These are just taxable brokerage accounts that hold our investments. There are no tax deferments and we would get taxed on our growth as well as our withdrawals. So how should we fit our three fund portfolio given these account options? Let’s look at another general rule of thumb to help us. The idea of tax efficiency when it comes to specific investments.

Tax Efficiency

There are naturally investments that are already “tax efficient” to begin with. Most often these are stocks and mutual funds that pay qualified dividends - dividends that receive favorable tax treatment. And stocks and mutual funds that avoid paying out taxable capital gains distributions. Such distributions are typical of actively managed funds that engage in frequent trading in their portfolios.

Vanguard Total Stock Market Index Fund checks the box on both of these thus is a great example of an already tax-efficient investment. The dividends it pays are modest and mostly “qualified.” And because trading (buying and selling) in the fund is rare, so too are taxable gains distributions.

On the other hand, investments that are “tax inefficient” are those that pay interest, non- qualified dividends and those that generate taxable capital gains distributions. Individual Stocks, Bonds, CDs and REITs fall into this category. And because of their tax inefficiency, we would ideally like to keep them in tax advantaged accounts that we talked about earlier, 401(k) and IRAs.

Slot Fund to Account

Alright, now that we have a good understanding of types of accounts and the concept of tax efficiency, let’s take a few steps back and slot our 3-fund portfolio into this framework.

As I mentioned earlier, Vanguard Total Stock Market Index Fund, the VTSAX is already tax efficient. Therefore, if we need to, it can fit into an ordinary brokerage account. It doesn’t mean it has to, but if we don’t have any more tax advantaged accounts remaining because we’ve maxed them all out, that it is ok to hold them in ordinary brokerage accounts. And this is the same with Vanguard Total International Stock Market Index Fund, the VTIAX.

The Total Bond Market Index Fund, VBLTX is not as tax efficient. Therefore you want to prioritize placing it in a tax advantaged account if you can.

Ofcourse, I want to reiterate, this concept only applies if you have already maxed out all your tax advantaged accounts. And when it comes to filling your tax advantaged account, the following would be my recommendation.

Tax Advantaged Accounts Order

First, fund your 401(k) plan to the full employer match. If your employer offers a 4% match, make sure to fund your 401(k) at minimum up to the 4% amount. This essentially is free money and you do not want to leave this on the table.

Second, fully fund your Roth IRA. Any money contributed to a Roth IRA grows tax free and you can withdraw tax free when you turn 59.5. Max it out if you can. The contribution limit per individual in 2022 is $6,000.

Third, if you have money left over, go back to your 401(k) and fund it to the max. Contributions to Traditional 401(k) lowers your taxable income and this is a no brainer way to pay less in taxes. The contribution limit per individual in 2022 is $20,500.

And only at this point, if you still have money left over, consider funding a taxable account. And this is where you can deploy the stock index fund in taxable vs. bond index in tax advantaged account strategy. Until you get to this point, I would recommend just funding your retirement accounts following your asset allocation.

Summary

Alright, I covered a lot in this post so let’s do a quick recap:

Step 1 - We want to select our three total market index funds. For Vanguard, this would be VTSAX, VTIAX and VBTLX.

Step 2 - We want to determine our ideal asset-allocation based on our risk tolerance.

Step 3 - We want to identify the best type of account(s) that is most tax advantageous to us. But most often this won’t apply until we’ve maxed out all our tax advantaged accounts first.

A final note that I want to share is that though I advocate for Vanguard in this video, Fidelity and Charles Schwab are now offering great low cost index funds as well. Of course all spurred on by the low cost bidding war that Vanguard started.

If you have a relationship with Fidelity or Charles Schwab already, also consider them to implement your 3-fund Portfolio. Fidelity now even offers a 0% total market index fund, the Fidelity® ZERO Total Market Index Fund. If you plan on staying with Fidelity for the rest of your life, it could be a great way to save a few dollars on your investment funds. If you like to learn more about my 5 favorite Fidelity funds to buy and hold forever, check out my post here.