Asset Allocation - What You Need To Know

When it comes to investing, it is very important to diversify your holdings. You don’t want to have all your money invested in one company or in one risky bet. This is why investing in low cost index funds like Vanguard Total Stock Market Index Fund, aka VTSAX is great because it automatically provides you diversification. However, smart investing doesn’t just end there. You want to take it one step further by allocating your money across different asset classes as well.

Stocks represent just one asset category. There are many other asset categories out there like bonds, commodities and cash. Investing in only one asset category over the long run can actually be quite risky. In essence, a well balanced and strong portfolio will not only be well diversified within an asset category, but also well allocated across multiple asset categories. Barbra Streisand said it best in her 1969 movie, Hello, Dolly!

“Money, pardon the expression, is like manure. It's not worth a thing unless it's spread around, encouraging young things to grow.” - Barbra Streisand, Hello Dolly! (1968)

Just like manure, spread your money around within an asset category and spread it around across different asset categories.

Why Is Asset Category Important?

So, you might be asking, why do we need to do this? I thought just purchasing a well diversified total market index fund is enough. Why do I need to purchase other asset categories as well? Well, the reason is because each asset category has different expected returns. Investing is by nature a risk taking endeavor. When you choose to invest in the stock market, you are believing that the stock market will appreciate in value because the companies within it will create value in the future. And higher risk you take, generally higher potential for reward down the line.

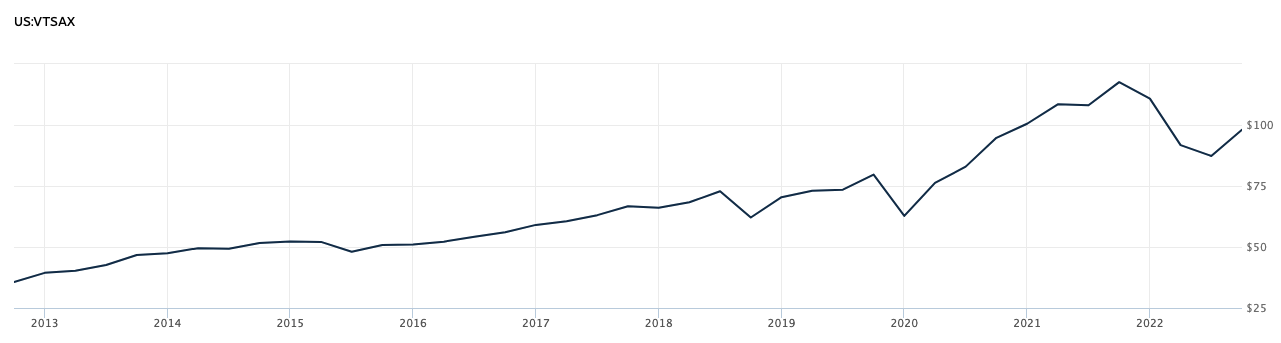

Because the stock market has generally appreciated in value in the last century, we automatically assume that the stock market is the only place we should invest our money in. Take a look at VTSAX for the last 10 years; the trend is up. However when you look closer at the 1 year trend, there are a lot of ups and downs throughout this upward journey.

VTSAX 10-Year (Upward Trend)

VTSAX 1-Year (Lots of Ups and Downs)

The market generally goes up in the long run, but it’s a pretty rough ride throughout. Think of a scenario where you are heavily invested only in stocks but for whatever reason the market tanks 30% next year. You were planning to start living off your investments, but now you can’t. You’ll literally be losing money if you start selling your investment now. You have to wait to see whether your money will climb back up - hopefully soon, but you’ll never know. You were taking a risk when you started investing in the market. This is the price of risk you have to pay.

Real World Consequences

And this theoretical scenario is actually not so theoretical. Lack of attention to appropriate asset allocation have and will continue to have an impact upon millions of Americans. In the last recession, many baby boomers saw catastrophic drops in their portfolios because they weren’t properly allocated. Those who were invested in all equities saw their net worth decline by double digits. Some sadly sold during the downturn because they needed the money, and by doing so, missed out on some amazing rebound over the next several years. You don’t want to be one of those in these situations.

Age & Risk

A key component to determining the appropriate asset allocation for you is your age and your risk tolerance. If you are in your twenties and have decades to grow your money, a portfolio made up of mostly stocks makes good sense. You have time to weather the storms, you can take the risk. So go heavy into stocks like the total market index fund. However, if you are older and retirement is coming up around the corner, you will want to taper back your risk.

Bonds - Counterweight to Stocks

And the way you can taper back your risk is by using Bonds. Bonds can act as your counterweight to stocks. Stocks and bond prices usually move in opposite directions. When the stock market is doing well, investors prefer the market over bonds, thus stock price goes up while bond demand drops.

However, when the stock market is not doing well and becomes risky for investors, investors withdraw their money and put it into bonds which they consider safer. This increased demand raises bond prices. By having bonds in your portfolio, they act as a buffer against you losing a sizable portion of your portfolio when the stock market tanks. So if you are in the later stages of your life and you want to reduce your risk, begin balancing your portfolio with bonds.

Suze Orman - 25 Million Reasons

Another scenario where really reducing your risk via more bonds makes sense is if you’ve accumulated a very large portfolio. Enough where you no longer need to expose yourself to unnecessary risk. In one famous example, Suze Orman, the famous personal finance expert was asked where she put her money. She said of her liquid net worth of $25 million, she only had $1 million in the stock market and the rest in bonds.

Given all the advice about investing in the market, the journalist who asked the question was shocked. How could she have so much money in bonds and not in the market. Suze said she had about 25 million good reasons that most people didn’t.

“Once you’ve won the game, there’s no reason to take unnecessary risk.” - Suze Orman

So, if you happen to have 25 million reasons like Suze Orman, having bonds in your portfolio might be a good option.

Typical Asset Allocations By Age

Alright, now that you understand why having bonds in your portfolio is important, let’s look how much might be appropriate for you. Just to give you a warning, the pursuit of perfect asset allocation is a heavily debated topic. And there is no one-size-fits-all approach to asset allocation as well as investing in general. I want to share with you sample allocation from Vanguard’s Target Retirement Funds. If you are hearing about Target Retirement Funds for the first time, check out my post here where I go deeper into it.

40-45 Years From Retirement: If you are in your twenties and are 40 to 45 years from retirement, you can see here how little bond you might need in your portfolio. Less than 10%. (VLXVX):

Vanguard Target Retirement 2065 Fund (VLXVX) Asset Allocation (Oct 2022)

10 Years From Retirement: However, as you get closer to your retirement age. Let’s say 10 years from retirement, you can increase your bond allocation to 35% of your portfolio to reduce your risk. (VTHRX):

Vanguard Target Retirement 2030 Fund (VTHRX) Asset Allocation (Oct 2022)

Retired: If you are already in retirement, bonds could make up 70% of your portfolio (VTINX).

Vanguard Target Retirement Income Fund (VTINX) Asset Allocation (Oct 2022)

One thing to note, these allocations are just a general rule of thumb. Some people might prefer to have 100% in stocks until they are in their 40s. Others are more conservative and want more money in bonds in their twenties - though I highly recommend against this since you have time on your side.

Asset Allocation Samples

Let me also share with you a few other popular asset allocations as a point of reference.

JL Collins - Simple, Aggressive Approach

JL Collins, the author of “Simple Path to Wealth” takes on a more aggressive approach with his asset allocation. He recommends when you are in your wealth accumulation phase, when you are still investing into the market, he recommends 100% in stocks. Specifically VTSAX - the total stock market index fund. He believes that you should be aggressive in your wealth accumulation phase, and I personally agree. You have time on your side and because you are in the accumulation phase, the market ups and downs don’t matter.

Now when you are in the wealth preservation phase, when you are living off your investments, he allocated his funds to following allocation:

75% Stocks (VTSAX)

20% Bonds (VBTLX)

5% Cash

Compared to the generic Vanguard Target Retirement fund asset allocation we saw earlier, this is definitely more aggressive. I personally like being more aggressive, but who knows a decade from now right? We all change and the great thing is our asset allocation can change with us as well.

Ray Dalio’s All Weather Portfolio.

Ray Dalio is a pretty famous Hedge Fund Manager and the founder of Bridgewater. Tony Robbins popularized this allocation method in his book “MONEY Master the Game.” The base of this allocation portfolio is that they believe it will do well in any market climate. And there’s a lot of support to that assumption given this portfolio is based on Bridgewater’s all season investing strategy. And in case you didn’t know, Bridgewater is the largest hedge fund in the world, with hundreds of billions in assets under management. And the general breakdown is as following:

30.00% Stocks

40.00% Long Term Bonds

15.00% Intermediate Bond

7.50% Commodities

7.50% Gold

Bit more complicated than Vanguards or JL Collins approach. I’m not showing you this allocation to say you should follow it, but to give you an example that there a lot of different flavors of asset allocation out there.

We Change, So Will Our Asset Allocation

But I want to share this with you. Asset allocation is important but for most people, the biggest danger in their investing journey isn’t if their portfolio is too aggressive or too conservative. It’s actually that people don’t invest enough or anything at all.

I’ve seen too many people who focus way too much time looking for the perfect fund and the ideal asset allocation, yet don’t have much money invested in the market. It’s important to understand the basics, but not to get too wrapped up in all the details. This can lead to analysis paralysis and keep you from the most important part of growing your wealth - saving and investing more money.

I believe that over time, we can all learn to manage our asset allocation as we get more proficient in investing and have a good understanding of our own risk tolerance. And know that it will change with time. You might be ok with being aggressive with your investments now, but when you have $25 million dollars in liquid assets like Suze Orman, your risk tolerance might change. Understand that appropriate Asset Allocation is a tool that will help you manage that risk.