Don't Overcomplicate Your Portfolio

Investing doesn’t have to be complicated. Most often three or even two index funds is all your need in your lifetime to grow your net worth. But we can’t help ourselves. We overengineer and overcomplicate even when a simple solution is good enough. You are passionate about investing and you want to do everything to maximize your returns.

You feel like small changes, regardless of how incremental and small they are, can make a big difference over time. And there is some validity to this statement. When looking at a mutual fund’s expense ratio, a difference between a 1% expense ratio versus a 0.1% expense ratio can cost you or earn you millions of dollars over decades due to compounding.

But are there some things that we just shouldn’t do? Are there portfolio complexities that we should just forget about because they have diminishing returns? Let’s cover a few of them in this article.

1 - Chase Returns

When I talk about investing, one of the most common questions I get is, how’s this investment’s returns compared to other similar investments? And I’m not just talking about individual stocks because that is a whole another conversation, but about broad market low cost index funds.

A good example of this is when we compare two very good index funds that I would recommend to anyone. A S&P 500 index fund and a total stock market index fund. Vanguard representative funds would be the Vanguard Total Stock Market Index Fund, also known as VTSAX and the Vanguard 500 Index Fund, also known as VFIAX.

I’ll be upfront with you. You can’t go wrong with either one of them. I like VTSAX, but that is just a personal preference. The key factor isn’t which one you choose, but how much you invest and for how long. Both will make you a millionaire in the long run.

But let’s say you are genuinely looking to understand which one is better. Well, let’s do a comparison exercise over different periods. The Vanguard website provides return data that goes back to the year 2000, but I want to go back a little further.

The Center for Research in Security Prices at the University of Chicago has gone back to 1926 and has actually calculated the returns earned by all US stocks since. Their data shows that the two indexes parallel one another with near precision.

According to this study, for the full period, the average annual return on the S&P 500 was 10.3% while the return on the Total Stock Market Index was 10.1%. You must be saying - alright, I got it, the S&P 500 is better. That’s where I should be putting my money.

But before you stop reading, let me share with you a few other interesting takeaways. When we go back specifically to VTSAX vs VFIAX, and you compare the returns between 2000 to now, interestingly the total market, VTSAX has better returns than the S&P 500, VFIAX. 7.25% vs. 6.93%.

Alright, are you thinking about changing your mind? Maybe the Total Stock Market is better. But wait, let me throw in another wrench in your decision. Take a look at the 10 year return. VFIAX has better returns at 12.75% vs. VTSAX’s 12.40%.

Are you confused yet? This represents what’s called a “period dependent outcome.” Everything depends on the starting and the ending date.

Going back to our historical chart, if the comparison began in 1930 instead of 1926, the returns between the two would be identical at 9.9%. The outcome really depends on which period we decide to look at. When you compare the past 20 years starting 2000, yes VTSAX has better returns - because small and mid cap companies performed better. But if you change the starting line to 10 years ago, VFIAX is better.

The bottom line is this. The long-term correlation on the returns between the two indexes is 0.99. 1.0 is perfect correlation. In the big picture of things, I personally think there is really little to choose between them.

And this is true for so many low cost index funds out there. VTSAX, VFIAX, VTI, VOO, FSKAX, FXAIX, SWTSX. All these are variations of the total market or the S&P 500, and you can’t go wrong with any of them. You just need to pick one and invest for the long run. Don’t try to chase returns with low cost index funds. Pick one and stick with it for the long run.

2 - Constantly Move Money Around

You might be comparing the returns between VTSAX and SWTSX and noticed that in the last 12.7 years there was a 0.02% difference in returns. So you decide that you want to move all your money to SWTSX because that 0.02% compounded over 30 years could make you an additional million dollars. My recommendation is don’t.

When we allow ourselves to constantly move money around, there might be some financial gains from it, but we are ignoring the emotional and time costs associated with it. Consider the time you are spending comparing the returns of these funds. And the time you are taking to actually open up an account with a new firm and to manage the process of moving your money around.

Yes, did the S&P 500 fund outperform the total stock market index fund the past 10 years? Based on data, yes. However, who is to say that will be the case in the next 10 years. When people overweight a certain segment of the market because he or she believes it will provide excess returns compared to the rest of the market, this is called portfolio tilt.

For example, Eugene Fama won the Nobel Prize in part for his research that showed that small-cap stocks and value stocks have historically outperformed large-cap and growth stocks, respectively. Based on this research many investors tried to increase their returns by tilting their portfolio towards small-cap or value stocks.

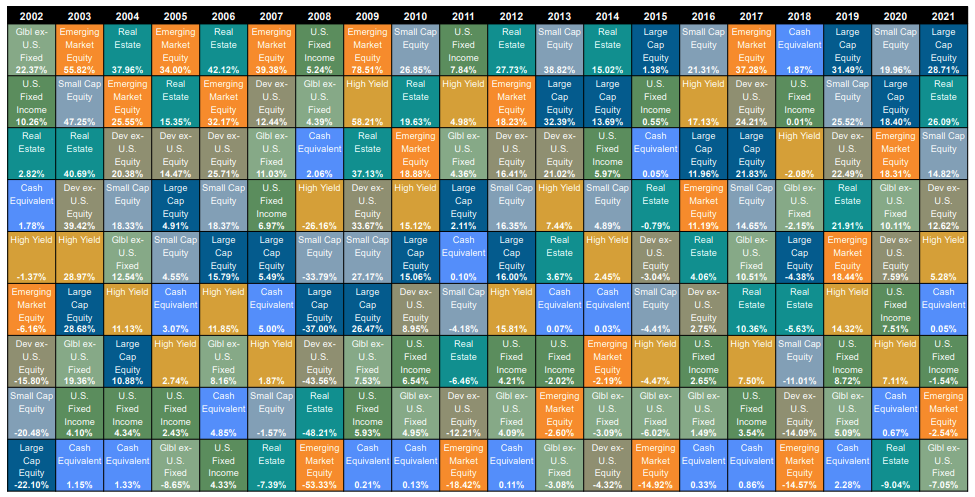

However, we just don’t know whether this outperformance will persist in the future. Past performance is not a guarantee of future returns. Take a look at the following Callan Periodic Table of Investment Returns. This chart graphically depicts annual returns for various asset classes, ranked from best to worst:

Callan Periodic Table of Investment Returns

You see times when large equity caps did well. You see times when small cap equity did well. And you even see times when real estate did well. What this table highlights is the inconsistency in the performance of different asset classes each year. Just because the large cap equity fund did well in one year doesn’t guarantee that it will continue to perform better than other asset classes the following year.

We want to resist the temptation to constantly move money around. As you saw in the earlier point, not only is chasing returns not effective, moving money around in pursuit of those returns is not the best use of your time.

3 - Constantly Tweak Asset Allocation

Asset allocation is one of the most important decisions you will make as an investor. If retirement is right around the corner you don’t want to have all your money in equity funds. The stock market’s volatility is unpredictable and you could find yourself needing to pull money out when the market has dipped by 20 to 30%. However, this doesn’t mean you should constantly tinker with it.

A general rule of thumb is that you should look at your asset allocation once a year. But that doesn’t mean you have to do anything every year if your percentages are pretty close to where you want it to be. Especially if you are in the wealth accumulation phase, you want to be heavily weighted towards equity anyways so there is no point in constantly looking at your asset allocation to verify that fact.

A good example of how people constantly tinker with their asset allocation even with a simple 3 fund portfolio is when it comes to international funds. A 3 fund portfolio advocates for 3 simple funds. And as its name implies, it is made of three simple index funds: a Total U.S. Equity, a Total U.S. Bond, and a Total International Equity fund.

Now a big debate amongst many individuals who pursue this strategy is how much international funds to hold in their portfolio. Unfortunately there is no sure fire answer to this question because so much of it depends on one’s worldview and appetite for international exposure.

However, ironically the swing on preference for international funds changes with the performance of international stocks. When international stocks are outperforming domestic stocks, you see more people saying that they are 30% or even 50% international stocks. When international stocks are doing poorly compared to the US companies, people run to the 2-fund camp that you don’t need international stocks.

Investors fall into the trap of jumping around from allocation to allocation. Holding international stocks after a period of outperformance and U.S. stocks after a period of international underperformance.

Asset allocation is important. But don’t overthink it. Come up with an allocation that works for you and stick with it. And if you are thinking about changing it, don’t switch it multiple times in a given year. At least give it a few years so you can rationally decide if it will work for you long term.

For me, given that I’m in my wealth accumulation phase my portfolio allocation is weighted heavily towards Total U.S. Equity and I hold a very small percentage in international and bond funds. I’m sure this will adjust with time, but I don’t plan on changing anything for at least many more years.

4 - Add Additional Asset Classes

As I mentioned earlier, the big three big asset classes are U.S. stocks, international stocks, and U.S. bonds. However, there are other minor asset classes such as emerging markets stocks, gold, oil, currencies, cryptocurrencies, real estate and many more too many to count. And as you can imagine many savvy investors can’t resist the temptation to do something cool and different from the crowd by dabbling in some of these other asset classes.

I remember having these feelings often when I first got started in investing. It was so hard for me to accept that after doing all the research of investing in the market the solution could be so simple and frankly boring. I felt like I wasn’t doing my intelligence justice by just following a simple 3 fund or a 2 fund strategy.

Yes, if your core holding is following the 3-fund strategy, dabbling a tiny percent of your money in new asset classes probably won’t make much difference. I like to use the 5% parameter. No more than 5% of my investments in new asset classes. And sometimes dabbling in new asset classes could help with your financial education by keeping you on your toes.

But the brutal fact is that even if you didn't touch any new asset classes for the rest of your life, it probably won’t make any appreciable difference in your overall returns. If you are living below your means, saving and investing a good portion of your income into the market you will eventually achieve financial independence and be able to retire comfortably.

Could you make a little bit more money by dabbling in currencies? Maybe. Could you hit it big by putting some of your money in angel investing? Potentially. When you achieve financial independence through the very boring 3-fund or 2-fund strategy, it won’t really matter how much additional returns your other asset classes brought in.

Research has shown, as we get wealthier additional money won’t make us any significantly happier once our basic needs are met. My recommendation is to keep things simple. Why over complicate our finances when a simple solution will get us to the finish line nonetheless.

Conclusion

The media likes to convey an image of investing as something sexy and complicated. However, the reality is that really effective investing is actually quite boring. I mean I like index funds, but even I admit that investing in a few index funds and holding for a long period of time is boring.

That is why it is so tempting to get swept up by the talks of our friends who are boasting about their latest Tesla stocks or bitcoins. We can’t help ourselves but think: can I squeeze out additional returns by adding new asset classes, adjusting my allocation or moving my money to a new investment firm? But remember Jack Bogle’s quote in simplicity.

“When there are multiple solutions to a problem, choose the simplest one.” - Jack Bogle

I firmly believe that in investing, as in other areas of life, the perfect is the enemy of the good. When we seek to maximize our portfolio returns with these tinkering, we are expending energy that could be used better elsewhere.